Is the Triple Play Working?

By Arthur Middleton Hughes

Many leaders of phone and cable TV companies have said that the “triple play” is

essential to successful customer acquisition and retention today. By the triple play, they mean that the same company offers and sells telephone, Internet broadband, and videoTV to its customers.

Why is this considered to be so important? The easiest to understand is the effect on

customer churn. It is known in many industries that customer churn is a function of the number of products owned by each customer.

The churn rate is the percentage of particular customers who defect each month. Suppose 100,000 subscribers have land lines from your company. Look now at those who have both land lines and broadband. Their churn rate will probably be lower. If you look further at those who have these two products plus a third one such as wireless or IPTV, you will note that these customers may have a still lower churn rate.

Churn is expensive. By churn we mean the switching by customers from one provider to

another to take advantage of lower prices or new features. It is expensive to acquire a

new customer. Sometimes it takes a year or more to pay off the cost of acquisition

through profits from subsequent purchases. When customers leave due to churn, the

acquisition cost is lost. So is future revenue.

To reduce churn, companies use a host of strategies. Some involve long-term contracts.

Others involve customer communications, or excellent customer service. As it turns out,

one of the most productive strategies is to sell the customer a second or third product.

This is particularly effective in reducing churn if the product prices are structured so that

the purchase of second and third products reduces the monthly price to the consumer of

the first product. Otherwise known as “bundling,” this tactic can also greatly reduce the

acquisition cost of the second and third product.

To create a bundled price system, the provider has to have several different products.

Banks have lots of different products: checking and savings accounts, credit cards, auto

loans, home equity loans, etc. Experience proves to them that the value of a second or

third product is more than the profit from that product. It also increases the increased

retention rate of the first product. Telephone companies in the past have typically had only one product: one or more land line phones. As long as the telephone company had a

monopoly on wired phone service, the annual retention rate was typically very high—at

least 95% or more.

Since wireless phones came along, the wired line churn rate has been growing. Some

wireless customers have found that they can do away with wired phones altogether. Add

to that competitive phone service provided by cable TV companies, or Internet

companies like Skype or Vonage, and the churn problem has become a major concern to

all phone companies. For example, Verizon sued Vonage for patent infringement and

won a $58 million plus 5% royalty verdict which is being appealed. Most press accounts

attributed this lawsuit to the intense competition between Vonage and land line phone

companies.

For several years, phone companies have been selling a second product: Internet

broadband using DSL. This is the double play. One problem with phone company

broadband has been that cable TV companies also offer Internet broadband, which,

because of their coaxial cables, is often much faster than what the telephone companies

have been able to provide. A more serious problem for phone companies is that cable TV

companies have begun offering telephone service as well as broadband: the triple play.

Cable TV companies have been stealing phone company customers by the millions in the

last few years through the triple play. Phone companies have decided that they have to

find a way to offer what the cable TV companies provide – video and TV — to keep their

customers.

There is no question today that in theory the triple play for a telephone company,

appropriately offered in a bundle, can be used to boost the retention rate or to reduce the

churn rate (which is the same thing). That is why telephone companies have been trying

to discover the most effective method of offering video-TV to their customers. The triple

play increases the retention rate. But what about customer acquisition?

Does the triple play improve the acquisition rate?

Do some consumers place a value on the idea of putting all their eggs in one basket? Do

they want to get phone, broadband and TV from the same company so much that their

purchase decision is swayed into choosing a triple play provider over buying phone

service from the phone company and TV service from a cable provider? Triple and

quadruple play assumes that a subscriber would want fixed and mobile voice with

broadband internet and Video-TV through a single, bundled subscription, at a lower price

than buying the services individually from different suppliers.

To see if this is true, we have to ask how do most consumers make their communication

vendor decisions? To begin with, we can divide customers into two categories: early

adopters, and mainstream buyers. Early adopters always want to try something new

before most people have even heard of it. They are the ones who will purchase phone

service from a cable TV company, or video-TV from a phone company. A small

percentage– say 10% — of all consumers are early adopters. The triple play might well

appeal to them. Telco and cable TV marketers should seek out early adopters and get

them to try and buy.

Looking at the rest of the consumers–the mainstream buyers –we can also divide them

into two categories: transaction buyers and relationship buyers. A transaction buyer is

interested mainly in price. Show them a way to save money, and they will go there.

Relationship buyers are not as interested in price. They are motivated by two ideas:

quality of service, and loyalty. They want a reliable provider who gives good customer

service. They do not care so much how much it costs as much as does it work well, is it

reliable, and do they treat me well?

For transaction buyers, a triple play bundle may be a great idea, and should work well. It

should reduce their costs. For relationship buyers the triple play may not work at all.

They may have Comcast in their living room providing TV, Verizon in their kitchen and

bedroom providing the phone service and AT&T as their wireless phone company. They

may not like the idea of deserting any one of these three tried and true providers in favor

of a bundle idea which forces them to leave old friends.

How are companies doing in selling the triple play? Pyramid Research (www.pyr.com)

reported that most Telcos are selling 1 to 1.5 revenue generating units (RGUs) per

customer while cable companies perform slightly better, selling around 1.5 to 1.9 RGUs

per customer. Time Warner Cable reported that only about 7% of their customers had

bought the triple play by 2007. CableVision, which ended up in 2006 in the red, however,

reported that over one third of their 3.1 million cable TV subscribers have bought the

triple play. Verizon had an RGU of 1.4 by the third quarter of 2006 – a year to year

growth of 1.1%.

Is the triple play profitable? Comcast’s CFO John Alchin said recently, “The triple play

really changes everything about our business and the way that we are marketing to our

customers. It’s important to take into account that we’re really presenting this to the

customers as a $33 value for each one of the products that we are offering.” The $99

package for all three products typically expands, he explained, with customer-requested upgrades, to between $120 and $130; pointing out that about 80% of those adding

Comcast Digital Voice are subscribing to all three of the company’s triple play products.

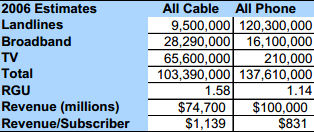

Overall, the triple play is working for cable. The following figures are only rough

estimates of the 8,500 cable TV systems and the 1,300 US landline phone systems. They

show that, if we ignore wireless, cable is doing better with the triple play than the phone

companies

What they show is that cable leads in broadband subscriber acquisition, as well as having

acquired nine and a half million phone customers compared to the phone companies

210,000 TV customers so far. In general, the cable company’s revenue per wired

subscriber is greater than that of the Telecos. The telephone companies are getting into

the triple play very late in the game. For a cable company that has already millions of

broadband customers, it is very easy, technically, to add phone subscribers using Voice

over Internet Protocol (VoIP). For the telephone company with two little copper wires

going in to a residence, adding television service is a very difficult assignment. Verizon

and AT&T are approaching the task in two completely different ways. Verizon with their

Fios system is laying fiber optic cable to three million homes per year (6 million so far).

Fiber is so powerful that each cable can provide a homeowner with enough bandwidth to

handle as many high definition TV sets, computers, and phone lines as any consumer

could possibly need. Despite this capability, Verizon has signed up only about 207,000

TV customers. AT&T with their U-Verse system is attempting to use advanced DSL to

provide TV to customers through the existing copper phone wires. They have only sold

3,000 consumers so far after a year of trying. In summary, selling the triple play

including TV for telephone companies is expensive and very difficult. For cable

companies, it is comparatively easy.

Where Telcos are accomplishing the triple play, however, is with wireless. Both Verizon

and AT&T own wireless companies that are expanding rapidly and are very profitable. If

done right, the triple play with wireless should work just as well as it does using TV as

the third play. This is undoubtedly a key reason why AT&T has renamed their Cingular

wireless system as AT&T.

Conclusion. The triple play is useful goal for any telecom seeking to increase profits.

RGU is a useful measurement for success in marketing. Some companies are doing a lot

better than others. By segmenting their subscribers into categories such as early adopters

and transaction buyers they may be able to concentrate on those consumers most likely to

buy the triple play.

==========================

Arthur Middleton Hughes is Vice President of the Database Marketing Institute

(www.dbmarketing.com) Arthur is the author of Strategic Database Marketing 3rd Ed.

(McGraw-Hill 2006) and a new book on Telecom Marketing to be published by Racom

Communications. He may be reached at [email protected]